EU €3 Customs Duty on Small Parcels: What Sellers Need to Know for July 2026

From 1 July 2026, the European Union will remove the long-standing customs duty relief for many low-value parcels and introduce a temporary customs duty of EUR 3 per item for consignments with an intrinsic value not exceeding EUR 150.

For cross-border ecommerce sellers, this is more than a small additional fee. It changes how low-value shipments should be costed, declared, routed, and explained to EU customers. It also sits inside a wider EU customs reform that is moving ecommerce imports toward more structured product data, clearer platform responsibilities, and a new EU Customs Data Hub.

The short answer: sellers that ship goods directly from outside the EU to EU consumers should review their EUR 150-and-under SKU economics now. The new duty may affect landed cost, delivery terms, IOSS workflows, customs declaration data, and the business case for EU-based fulfilment.

What is changing on 1 July 2026?

Until 1 July 2026, goods in consignments with a total intrinsic value not exceeding EUR 150 can generally benefit from customs duty relief, although import VAT still applies and customs declarations are still required.

Council Regulation (EU) 2026/382 deletes that threshold-based customs duty relief. From 1 July 2026 until 1 July 2028, a temporary customs duty of EUR 3 per item applies in a consignment whose intrinsic value does not exceed EUR 150, where the goods fall within the scope set out in the regulation, including IOSS-related imports or postal consignments.

In practical terms, the rule is not simply “EUR 3 per parcel.” The European Commission guidance explains that the automatic calculation is based on declaration lines: the number of declaration lines entered in the customs declaration multiplied by EUR 3. The Q&A further clarifies that operators should use one line per goods sharing tariff classification in H7 declarations.

That means a parcel containing multiple goods may trigger more than one EUR 3 duty amount if the goods must be declared on separate item lines. Sellers should avoid simplifying this as a flat parcel fee in customer-facing or operational content.

Who is most likely to be affected?

The change is most relevant to businesses shipping low-value goods from outside the EU to EU consumers, including:

- Independent ecommerce brands shipping directly from non-EU warehouses.

- Marketplace sellers using channels such as Amazon, eBay, AliExpress, Temu, SHEIN, or other platforms, depending on the fulfilment model.

- Shopify, WooCommerce, and DTC sellers using postal or express parcel networks.

- Logistics providers, customs brokers, and fulfilment partners handling high volumes of low-value EU-bound parcels.

- EU consumers who may ultimately see higher landed prices or more transparent checkout charges.

The impact will vary by product mix and logistics model. A seller shipping one low-margin accessory per parcel will experience the duty differently from a seller shipping higher-margin goods or consolidated assortments with clean declaration data.

Why is the EU making this change?

The EU frames the change as part of a broader customs reform rather than an isolated fee increase. The European Commission says the reform responds to ecommerce growth, the rising number of EU standards that customs must check at the border, and the need for a more data-driven customs system.

The Council regulation also points to misuse of the existing EUR 150 relief, including undervaluation and artificial splitting of consignments. Removing the relief is intended to protect public revenue, reduce unfair advantages, and support more consistent customs controls for ecommerce imports.

The wider reform also plans a more modern approach to ecommerce, including stronger responsibilities for online platforms and the EU Customs Data Hub, which the Commission says is expected to open for ecommerce consignments in 2028.

How does the EUR 3 duty interact with IOSS and VAT?

IOSS is not abolished by this rule. The Import One Stop Shop (IOSS) remains a VAT simplification for distance sales of imported low-value goods not exceeding EUR 150. It simplifies the declaration and payment of import VAT. The new EUR 3 amount is a customs duty, not VAT.

The European Commission guidance states that the deletion of the customs duty relief does not impact VAT schemes and rules related to distance sales. At the same time, goods imported using IOSS can still be subject to the EUR 3 customs duty under Regulation (EU) 2026/382.

For sellers, this means the workflow should not be described as “IOSS replaces the duty” or “the duty can be paid through VAT returns.” Instead, treat VAT and customs duty as separate obligations that must be reconciled through consistent product, value, and declaration data.

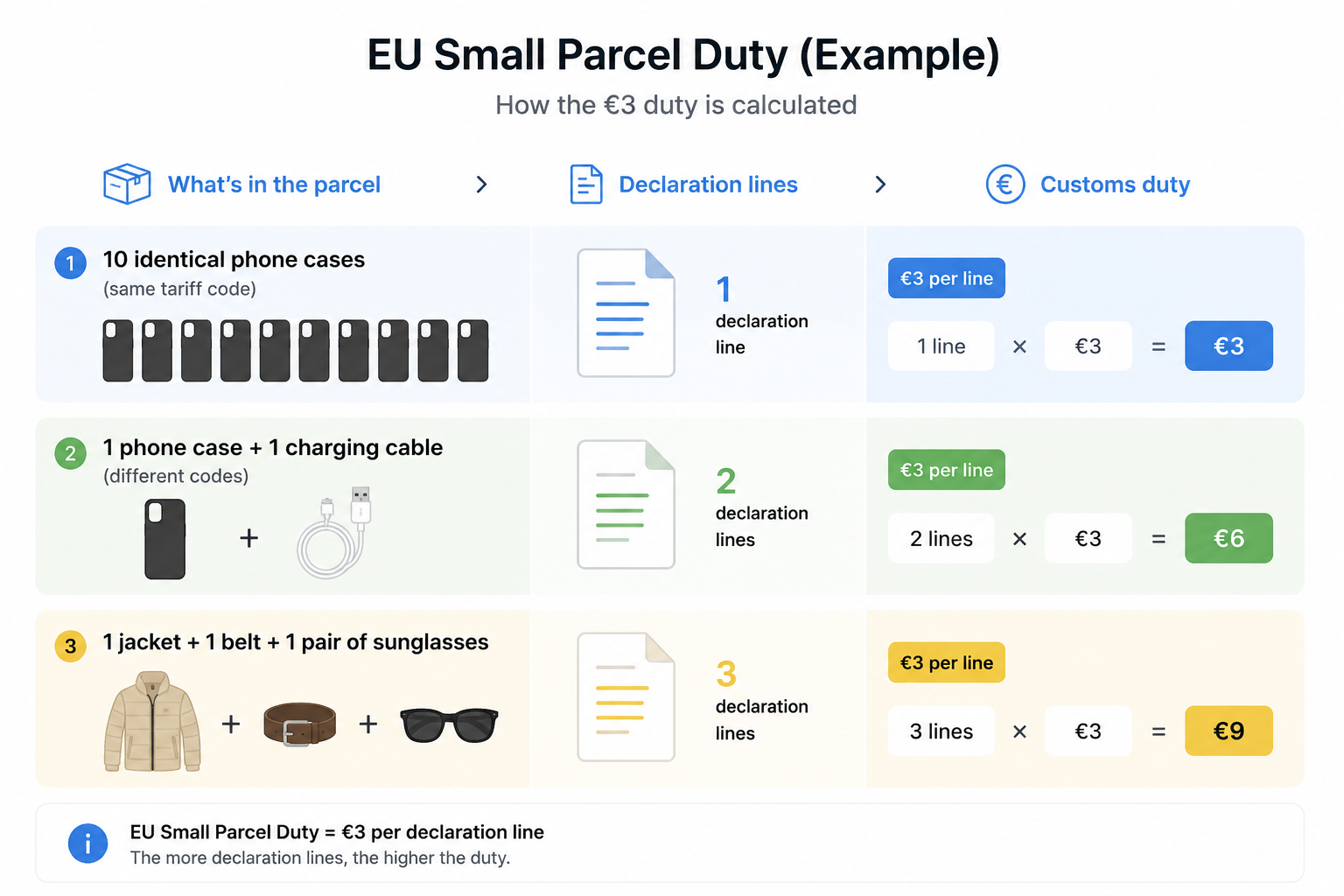

How Is the €3 Calculated? It Is Not Simply Per Parcel

The most important thing to understand about this rule is that the charge is based on declaration lines, not on the number of parcels. The payable amount equals the number of lines on the customs declaration, multiplied by €3. When goods share the same tariff classification, they can be grouped onto one declaration line — producing a single €3 charge regardless of how many units are in the parcel. When goods have different tariff classifications, they need separate lines, each attracting €3.

Here is how that looks in practice:

There is an important nuance: even if two items share the same tariff code, if they end up on separate declaration lines — perhaps because your carrier splits them — each line still attracts €3. The Commission guidance confirms this: the €3 applies per declaration line, irrespective of quantity, due to current IT system limitations.

This means that how your carrier or customs broker structures your declarations directly affects what you pay. Confirm the declaration line approach with your logistics provider before 1 July. Do not assume the charge will always be just €3 per parcel.

National Fees on Top: What Some EU Countries Are Adding

The EU-wide €3 customs charge may not be the only additional cost sellers face.

Several EU member states have already introduced or are considering introducing their own national handling fees. These charges apply in addition to the EU-wide levy, increasing the overall import cost of each shipment.

- France: €2 per unique HS6 item category (effective from 1 March 2026)

- Italy: €2 per consignment (effective from 1 July 2026)

- Romania: 25 RON (approx. €5) per parcel (effective from January 2026)

- Netherlands: Proposed fee of approximately €2 per parcel (currently postponed)

For example, a parcel shipped to France containing one jacket would incur €3 (EU charge) + €2 (French fee) = €5 in additional charges.

However, these country-specific fees may differ by implementation date, parcel type, carrier, declaration model, and national rules. They may also change as the EU customs reform is implemented. Sellers should therefore verify the latest requirements with their customs broker, logistics provider, marketplace, or the relevant national customs authority before updating checkout prices or customer-facing duty messages.

What sellers should check now

1. Identify affected SKUs and order flows

Start with a clean export of EU-bound orders and SKUs with an intrinsic value not exceeding EUR 150. Group them by product category, HS code, country of origin, fulfilment location, delivery method, and marketplace or storefront.

The immediate goal is to estimate where the EUR 3-per-item calculation may materially change margin or customer experience. Low-value, low-margin, multi-line orders deserve special attention.

2. Recalculate landed cost

Update landed-cost models to include:

- The EUR 3 customs duty where applicable.

- mport VAT.

- Brokerage, handling, or postal charges.

- Marketplace or logistics collection fees.

- Returns and refusal risk.

- Potential operational costs for product identifiers, better item data, and reconciliation.

Do not model the rule only as a parcel surcharge. Where separate declaration lines are needed, the cost may be higher than EUR 3 for a single parcel.

3. Review DAP and DDP delivery terms

Check whether current delivery terms create a poor buyer experience after the new duty begins.

DAP means Delivered at Place. Under a DAP model, the buyer may be responsible for import charges when the parcel arrives, depending on the arrangement. That can increase refusal, support tickets, and negative reviews if checkout messaging is unclear.

DDP means Delivered Duty Paid. Under a DDP model, the seller is responsible for arranging payment of duties and taxes so the buyer receives a more predictable landed price. DDP may improve customer experience, but it can also require stronger customs broker, pricing, and reconciliation processes.

Sellers should confirm the exact Incoterms and charging flow with logistics providers rather than relying on internal shorthand.

4. Improve customs declaration data

Weak product data will become more expensive. Review:

- HS or CN classification.

- Product description.

- Intrinsic value.

- Country of origin.

- Quantity and declaration line structure.

- Product identifiers where required.

- Marketplace or seller product IDs.

Avoid vague descriptions such as “gift,” “accessory,” or “daily use item.” Poor declarations can delay clearance and increase inspection risk.

5. Re-evaluate EU fulfilment

EU-based warehousing may become more attractive for some sellers, especially when direct shipping is slow, low-margin, or operationally fragile. However, sellers should not assume that an “EU warehouse” automatically removes all customs obligations.

Goods imported into the EU must still be properly declared when they are released for free circulation. Once goods are lawfully imported and sold from EU stock, the later domestic or intra-EU customer delivery is a different flow from a non-EU direct-to-consumer parcel.

The right model depends on sales volume, product category, VAT registrations, storage costs, import responsibilities, returns, and marketplace strategy.

6. Update customer messaging before checkout

If customers may face import charges or delivery-term changes, update:

- Shipping policy pages.

- Checkout tax and duty messaging.

- Marketplace listing templates.

- Help-center articles.

- Delivery confirmation emails.

- Customer-service scripts.

The safest messaging is precise and calm: explain what may be charged, when it may be charged, and who collects it. Avoid vague warnings that create fear without operational clarity.

FAQ

Is the EUR 150 threshold completely gone?

The customs duty relief threshold is being removed. The EUR 150 value still matters for determining the scope of the temporary EUR 3 duty and for VAT/IOSS-related processes.

Is the EUR 3 charge per parcel or per item?

The regulation says EUR 3 per item in a consignment with intrinsic value not exceeding EUR 150. Commission guidance explains that, for automatic calculation, the payable amount equals the number of declaration lines multiplied by EUR 3. Operators should structure declaration lines according to the applicable rules for goods sharing tariff classification, description, and origin.

Does IOSS still apply?

Yes. IOSS remains a VAT simplification for distance sales of imported goods not exceeding EUR 150. The EUR 3 customs duty is separate from VAT and should not be described as payable through an IOSS VAT return.

Will the rule last forever?

The transitional EUR 3 duty applies from 1 July 2026 until 1 July 2028. The regulation also requires the Commission to assess whether trade-flow diversion occurs and whether the centralised EU IT infrastructure will be operational by 1 July 2028. If the infrastructure is not expected to be ready, the Commission may propose extending the transitional measure.

What should sellers do first?

Start with a SKU and order-flow audit. Identify direct-to-EU shipments with intrinsic value not exceeding EUR 150, model the duty by declaration line, and confirm IOSS, DAP/DDP, customs broker, and marketplace processes before 1 July 2026.

This article is for general information only and does not constitute customs or legal advice. Sellers should confirm obligations with their customs broker, logistics provider, marketplace, or professional adviser before changing pricing, declarations, or delivery terms.

How VATAi can help

The EU's evolving small parcel duty rules are reshaping how e-commerce businesses import and sell goods across Europe. Keeping up with customs, VAT, and compliance obligations can be challenging—especially for sellers operating in multiple markets.

VATAi helps e-commerce businesses navigate these changes with confidence by providing end-to-end compliance support, including:

● VAT Registration & Filing – Obtain and manage VAT registrations across Europe and beyond, ensure ongoing filing compliance in all relevant markets.

● OSS Compliance Support – Understand whether the One-Stop Shop (OSS) schemes apply to your business and streamline your cross-border VAT obligations.

● EPR & Product Compliance Services – Stay compliant with EPR, GPSR, and other regulatory requirements when selling products in the EU.

● Dedicated Compliance Experts – Work with local tax and compliance specialists who can guide you through regulatory changes and help minimize compliance risks.

● All-in-One Compliance Platform – Manage registrations, filings, deadlines, and tax documents through one centralized platform designed for global e-commerce sellers.

As EU regulations continue to evolve, VATAi enables e-commerce businesses to stay compliant, reduce operational complexity, and focus on growing their sales across Europe.

Official Sources

1) European Commission, EU Customs Reform: https://taxation-customs.ec.europa.eu/customs/eu-customs-reform_en

2) Council Regulation (EU) 2026/382: https://eur-lex.europa.eu/eli/reg/2026/382/oj/eng

3) European Commission, Guidance on the EUR 3 customs duty: https://taxation-customs.ec.europa.eu/document/download/053e5b4e-f0be-4f20-9a23-3e3b659a6676_en?filename=Customs+Guidance+on+EUR+3+customs+duty.pdf

4) European Commission, Questions and answers on EUR 3 customs duty guidance: https://taxation-customs.ec.europa.eu/document/download/8350b1aa-935a-4b80-a349-385b36292fbe_en?filename=Questions+and+answers+on+3+EUR+Guidance+MS+and+Economic+operators_clean15062026.pdf

5) European Commission, VAT One Stop Shop: https://vat-one-stop-shop.ec.europa.eu/index_en

Need Help with VAT Compliance?

Book a free call with VAT Ai today to find tailored solutions for your e-commerce business

![]()